Buffered Annuities – A Strategy in Volatile Markets

Volatility – it’s a term we’ve heard a lot in the media and felt in the markets recently.

If you’re in the accumulation phase, you may view volatility as opportunity. But as you get closer to retirement, this viewpoint may shift more to uncertainty. Volatile times like these are when it can be most valuable to work with a Financial Advisor. By taking the time to understand your needs, your advisor can help you manage your emotions and create investment strategies tailored to your specific goals and risk tolerance. If you’re a risk-averse investor, you likely value investments that allow you to dial back risk in order to reduce potential losses, while if you’re less risk averse, you may be willing to take on more risk in exchange for the potential of a greater reward.

“So how can I reduce portfolio risk during volatile times?”

Buffered Annuities

Buffered annuities are a relatively new tool that allow contract owners to participate in some of the upside of the market while having a limited level of protection from market losses (subject to the claims-paying ability of the issuing insurance company). Their performance is linked to the performance of a market index (there are multiple indexes from which to choose) and the selected protection level. It is important to understand that, in exchange for the loss protection, the upside potential of the account value will be limited.Buffered annuities can be tailored to your needs by answering three questions:

- Which index (or indexes) do you want to track?

• Products/carriers offer many different indexes, but among the more commonly available are the S&P 500 Index (large cap), Russell 2000 Index (small cap), and MSCI EAFE Index (international stocks). - How much protection do you want?

• Products/carriers offer many different protection levels, but among the more commonly available are a -10% performance buffer and a -10% floor buffer. - How long do you want to invest?

• Products/carriers offer different surrender periods and index segments. Generally, most buffered annuities have a three-year or six-year surrender period with one-year, three-year, or six-year indexing segments. A “surrender period” is how long you must hold the annuity contract before you can fully access the account value without penalty. An “index segment” is how often the insurance carrier measures the chosen index to credit interest to your account value.

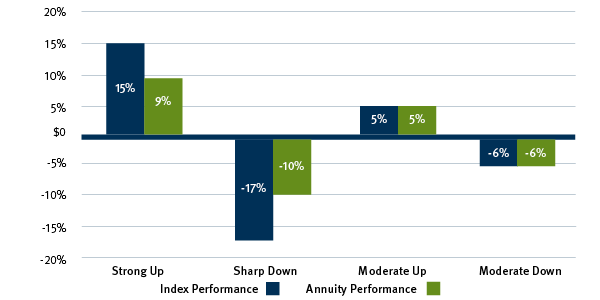

PERFORMANCE BUFFER STRATEGY

Examples in Different Market Conditions

|

Buffered Annuity With Floor Strategy |

| Participation Rate: 100% Cap Rate: 11% Performance Buffer: -10% |

| REMINDER |

|

This strategy participates in the upside of the index to the "cap rate" and is protected from any index losses up to the "performance buffer." |

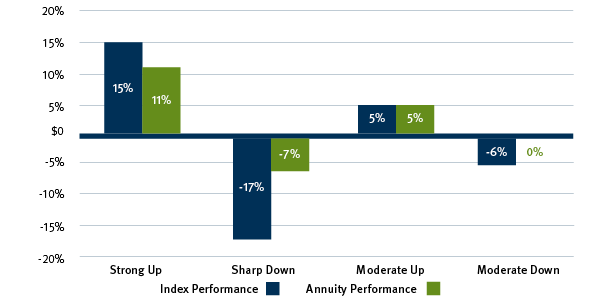

FLOOR BUFFER STRATEGY

Examples in Different Market Conditions

|

Buffered Annuity With Performance Strategy |

| Participation Rate: 100% Cap Rate: 9% Performance Buffer: -10% |

| REMINDER |

| This strategy participates in the upside of the index to the "cap rate" with a defined maximum loss potential equal to "floor buffer." |

The charts above are for illustrative purposes and do not reflect any specific buffered annuity product. Buffer protection levels, cap rates, and participation rates vary by product and insurance company and may be changed periodically at the discretion of the insurance company. Consult the product prospectus and discuss all associated risks with your Financial Advisor prior to making a decision to purchase any annuity product.

Important Information

Investors should obtain a prospectus for an annuity’s contract and the underlying subaccounts and consider the investment objective, risks, charges, and expenses carefully before investing. The prospectus, which contains this and other important information, is available from your Financial Advisor and should be read carefully before investing.

Buffered annuities are complex insurance and investment vehicles and are also known as indexed variable annuities (IVA) or registered index-linked annuities (RILA). Annuities are long-term investment products designed for retirement purposes that offer tax-deferred growth with access to lifetime income and/or death benefit protection. To decide if a buffered annuity is right for you, consider that its value will fluctuate; it is subject to investment risk and possible loss of principal; and, depending on the product selected, there may be costs associated with them which may include morality and expense charges, administration fees, and/or optional benefit(s) charges.Please reference the product prospectus for information about the levels of protection available and other important product information.

Surrender charges will apply for early withdrawals. Withdrawals are also subject to ordinary income tax treatment and, if taken prior to age 59½ in nonqualified contracts, may be subject to an additional 10% federal tax. There is no additional tax-deferral benefit for an annuity contract purchased in an IRA or other tax-qualified plan.

The risk of loss in a buffered annuity occurs each time you move into a new indexing term. The protection level option selected in the indexed account helps protect you from some downside risk. However, if the negative return is in excess of the protection level selected, there is a risk of loss of principal. Protection levels vary based on the product, index, and term selected and are subject to change at each insurance company’s discretion. Please see the product prospectus for details.

All contractual guarantees are subject to the claims-paying ability of the issuing insurance company, including payment from the indexed accounts, optional benefit(s) protections, fixed subaccount crediting rates, or annuity payout rates. Annuities are not backed by the broker-dealer or insurance agency from which the annuity is purchased, or any affiliates of those entities, and none makes any representations or guarantees regarding the claims-paying ability of the issuer. Annuities are not insured by the FDIC or any government agency.

Buffered annuity products and features are not available in all states or through all broker-dealers. Please consult with your Financial Advisor for more details on state approvals and broker-dealer availability.

1121.3020914.2